Oceanagold Provides Multi-year Outlook And Completes Haile Mine Technical Review

Photo Courtesy: OceanaGold Philippines

TSX: OGC

www.oceanagold.com

Mr. Gerard Bond reports:

(All financial figures in US Dollars unless otherwise stated)

BRISBANE, Australia, Feb. 9, 2022 /CNW/ – OceanaGold Corporation (TSX: OGC) (ASX: OGC) (the “Company”) is pleased to provide a three-year outlook of its forecast production, costs and capital requirements, including a detailed guidance for 2022. The Company has also completed the Technical Review of its Haile Gold Mine and, following a review of the carrying value of its assets in accordance with relevant accounting standards, the Company expects to incur a non-cash post-tax impairment charge of $102 million in its 31 December 2021 financial statements. This includes a non-cash post tax impairment charge of $181 million related to the Haile operation and a non-cash post tax impairment reversal of $79 million to fully reinstate the carrying value of the Didipio operation.

Highlights

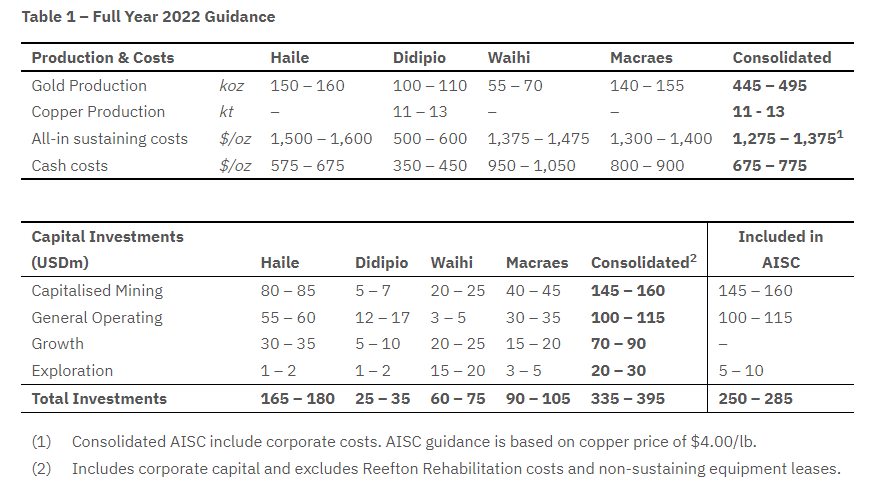

- Consolidated 2022 gold production guidance of 445,000 to 495,000 ounces and 11,000 to 13,000 tonnes of copper.

- Consolidated 2022 AISC guidance of $1,275 to $1,375 per ounce sold including cash costs between $675 to $775 per ounce sold, both on a by-product basis.

- Didipio 2022 production guidance range near full production levels at 100,000 to 110,000 ounces of gold along with 11,000 to 13,000 tonnes of copper.

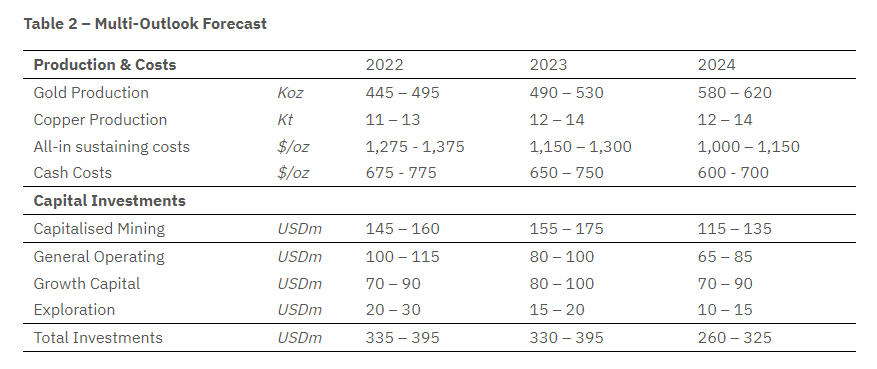

- Multi-year consolidated gold production of:

- 490,000 to 530,000 ounces plus 12,000 to 14,000 tonnes of copper at an AISC of $1,150 to $1,300 per ounce sold in 2023; and

- 580,000 to 620,000 ounces plus 12,000 to 14,000 tonnes of copper at an AISC of $1,000 to $1,150 per ounce sold in 2024.

- No material impact on Haile Mineral Reserves or Resources as a result of Technical Review.

Scott Sullivan, Acting CEO of OceanaGold said, “OceanaGold has a bright future. Over the next three years, we expect to increase gold production by approximately 70% compared with 2021, representing a compounded annual growth rate of approximately 15%. More importantly, we are expecting increasing free cash flow margins, particularly in 2024 with the step change in production and a decrease in capital investments. Additionally, copper production is expected to increase to steady-state production levels beyond this year as Didipio has ramped-up well ahead of expectations.”

“We have completed the Haile Technical Review which assessed the mine plan utilising updated operating and capital costs based on historic data, expected performance going forward and changes to our cost structure. Based on the Technical Review the Company did not reclassify mineral reserves and resources, although recognises the mine faces higher life of mine operating costs particularly in mining along with increased capital requirements related to waste stripping, Potential Acid Generating (“PAG”) storage and Tailing Storage Facility (“TSF”) expansion. Higher operating costs also includes the continued inefficiencies related to the re-handle of waste material due to delays in the Supplemental Environment Impact Statement (“SEIS”) and increased water management resulting from higher than normal wet seasons in 2018 and 2019. These costs are expected to stabilise over the course of 18 to 24 months following the receipt of the permits associated with a SEIS Final Record of Decision (“RoD”).”

“I am confident in the future of the Company and we are focused on rebuilding our credibility with the market as we continue to deliver on our commitments. Although the Haile Technical Review is complete, we see further opportunities to drive value and we are pursuing those. We will continue to drive productivity and cost efficiencies at all of our operations and particularly, we will build capability in our capital allocation program.”

Haile Gold Mine – United States

Haile Gold Mine – United States

In 2022, the Haile operation is expected to produce between 150,000 and 160,000 ounces of gold at cash costs of $575 to $675 per ounce sold, and AISC between $1,500 to $1,600 per ounce sold. As previously flagged, the delay in the SEIS RoD and associated permits is impacting mine efficiencies resulting in lower mining rates, reduced productivity, and higher costs related to additional re-handle of waste material. The Company currently assumes receipt of the SEIS in the first quarter of this year, allowing for the construction of additional waste storage facilities necessary for future waste storage needs. Additionally, the SEIS allows the Company to increase water discharge rates which is needed to reduce site water levels more efficiently, and to commence development at the Haile underground mine that will increase high grade ore feed in future years. Haile’s 2022 production profile is evenly weighted between the first and second halves however, first and fourth quarter production will be materially higher than the second and third quarters. AISC will correspond to quarterly sales volumes. Capital investments are expected to be the highest through the second and third quarters, based on the Company receiving the SEIS and associated permits in the first quarter. In 2022, capital expenditure of approximately $65 to $75 million ($35 – $40 million sustaining and $30 – $35 million growth) is contingent on receipt of the SEIS, with the start of spend planned in the second quarter.

Beyond 2022, production is expected increase marginally in 2023 and then increase significantly with higher grade ore feed from the underground in 2024. Operating costs and capital costs are expected to decrease over 2023 and 2024.

Haile Mine Technical Review

The Company has completed a comprehensive Technical Review of its Haile operation. This full review was carried out to optimise the long-term value of the asset. It addressed continued operational challenges including productivity inefficiencies, higher costs, additional capital requirements and operating constraints. Additionally, the Company evaluated an appropriate mine cut-off grade based on the expected cost structure and future capital requirements. As a result, the cut-off grade was increased from 0.45 g/t gold to 0.5 g/t gold. Despite the increase to the cut-off grade, it was determined that Haile’s Mineral Reserves were economic and as such, remain in the mine plan with no changes other than factoring in mine depletion and the change in cut-off grade.

Haile is expected to produce approximately 2.1 million ounces of gold over a mine life out to 2034. The average LOM AISC is approximately $1,080 per ounce while cast costs average approximately $700 per ounce.

Following completion of the Technical Review, the Company completed a review of the carrying value of the Haile mine in accordance with relevant accounting standards and expects to recognise a non-cash after-tax impairment charge of $181 million in its 31 December 2021 financial statements. The main driver for this decrease is higher open pit life of mine unit costs, particularly in mining where the Company currently forecasts open pit unit costs to average $2.48 per tonne inclusive of capitalised stripping. This compares to life of mine open pit mining unit costs of $2.00 per tonne mined assumed in the previous National Instrument 43-101 Technical Report (“Technical Report”) from September 2020. Processing unit costs are now assumed to average $11.64 per tonne milled compared to $9.98 per tonne milled in the September 2020 Technical Report while site G&A is now expected to be $4.89 per tonne milled over life of mine, compared to the previous estimate of $3.48. The processing costs include the costs of the water treatment plant.

In addition, the Company expects capital costs over life of mine to be higher than in the previous Technical Report. Sustaining capital costs, which are driven by increased pre-stripping cost and additional PAG storage requirements, are expected to be $750 million over the life of mine, averaging $115 million per year from 2022 to 2026 inclusive. This compares to $411 million estimated from 2022 over the LOM in the previous Technical Report. Growth capital going forward is predominately related to the development of the Haile Underground mine. Growth capital, including site closure costs, expected over life of mine is now $155 million compared to $145 million in the previous Technical Report.

Under the revised mine plan, mining operations will include the addition of RC grade control drilling with 25,000 metres of drilling expected in 2022, increasing to 50,000 metres in 2023. Grade control drilling is expected to reduce uncertainty, reduce dilution and allow the operation to mine more selectively. Open pit equipment productivity estimates have been revised based on operational history and benchmarking. These changes will result in decreased annual material movement rates relative to the previous mine plan. A blast fragmentation optimisation plan was implemented in the third quarter of 2021 and yielded positive results including higher throughput through the mill. The Company will continue to optimise blast fragmentation, including waste areas, which is expected to deliver further operational improvements.

The Technical Review has resulted in a reduction in milled tonnes per year and the Company now expects Haile to achieve an annual mill feed of 3.6 to 3.7 million tonnes from 2022 to 2027 increasing to 3.8 million tonnes from 2028 onward. The decrease is related to ore hardness and the bottleneck at the Semi Autogenous Grinding mill, but it is offset partially by blast fragmentation optimisation. Additionally, the operation now expects life of mine recoveries to average 81% with potential opportunities to increase through future improvement initiatives requiring no additional capital.

The Haile operation will continue to seek opportunities to further improve the new mine plan to drive higher productivities while decreasing costs and capital. The Company expects to release an updated Haile Technical report by the end of the first quarter.

SEIS Update

The Company continues to expect the SEIS ROD in the first quarter and anticipates receipt of subsequent operating permits shortly thereafter. The permits are necessary to allow underground mine development and expansion of the operating footprint to accommodate the construction of future PAG waste storage facilities and increased water discharge rates. As previously guided, the ongoing delay in the finalisation of the SEIS is impacting productivity at Haile, where mining rates are limited by additional material and water re-handling, reducing output, and increasing costs. Upon receipt of the necessary permits, the Company has plans to improve operational efficiency with fewer constraints and lower mining unit costs to be delivered progressively over a two-year period. The Technical Review has assumed receipt of the necessary permits related to the SEIS in the first quarter with some provisions in place should further delays be experienced.

Didipio Gold-Copper Mine – Philippines

Ramp-up of the Didipio operation continues to progress ahead of schedule. The Company now expects to reach full underground production rates early in Q2 2022 and, as a result, expects full year production of between 100,000 and 110,000 ounces of gold along with 11,000 to 13,000 tonnes of copper. For the full year, Didipio’s by-product AISC is expected to range between $500 to $600 per ounce sold, while by-product cash costs are expected to range between $350 to $400 per ounce sold.

For 2022, Didipio’s capital requirements are primarily related to capitalised underground mining and general operating costs related to plant upgrades and the TSF lift. Didipio will continue to sustain modest growth capital ranging between $5 to $10 million per year related to the continued build-out of panel two of the underground mine. The Company will resume drilling of the Didipio ore body in 2022 with an aim to extend mine life through discoveries at depth. Greenfield exploration activities are expected to resume late in 2022 on near-mine targets.

Beyond 2022, Didipio is expected to produce between 110,000 and 120,000 ounces of gold per year along with 12,000 to 14,000 tonnes of copper per year at similar AISC and cash costs.

With Didipio operations now resumed, the Company has assessed the carrying value of the asset in accordance with relevant accounting standards. As a result, the Company expects to reverse the previous impairment charge recognised and increase the carrying value of Didipio by $79 million as at December 31, 2021.

Waihi Gold Mine – New Zealand

The ramp-up of the Martha Underground is expected to continue over the next two years with gold production achieving full production rates in 2023. For 2022, the Waihi operation is expected to produce between 55,000 and 70,000 ounces of gold, a significant increase over 2021. This is related to additional mine faces to be brought online at Martha Underground. The Company has elected to use a wider guidance range for the Waihi operation because of continued risks related to COVID-19 and ongoing discrepancies between mined grades and the resource model. The Company will continue to progress resource definition and grade control drilling to update the resource model. Consolidated AISC is expected to range between $1,375 and $1,475 per ounce sold with cash costs between $950 and $1,050 per ounce sold. Production in the second half of the year is expected to be stronger than in the first half with the fourth quarter expected to be the strongest quarter of production at a lower corresponding AISC.

Waihi’s capital requirements are primarily related to the continued ramp-up and development of the Martha Underground mine and advancement of the Waihi North Project (“WNP”). The latter is mainly focused on advancing the Wharekirauponga (“WKP”) prospect ten kilometres north of the Waihi process plant. For 2022, the Company expects to invest between $15 and $20 million in exploration with approximately half of this expenditure associated with infill and expansionary drilling at WKP where the Company expects to drill 15,000 metres.

The Company anticipates lodging the formal consenting application related to WNP in the first half of 2022. The consenting process continues to be the critical path to commencing development of WNP deposits including WKP. In the meantime, technical study work on WKP will continue through 2022 and 2023 with an expanded scope of work and additional drilling planned to optimise mine and infrastructure design.

Beyond 2022, the Waihi operation is expected to produce between 90,000 and 100,000 ounces of gold per year at lower corresponding AISC and cash costs. Sustaining capital requirements in 2023 and 2024 are expected to remain at similar levels while growth capital increases in 2024 with the development of WNP associated projects.

Macraes Gold Mine – New Zealand

In 2022, Macraes is expected to produce between 140,000 and 155,000 ounces of gold at an AISC of $1,300 to $1,400 per ounce sold and cash costs of $800 to $900 per ounce sold. The wider production guidance range reflects uncertainty related to potential COVID-19 restrictions as the New Zealand government continues to seek to supress cases with international borders expected to remain closed until at least mid-2022. Production for the year is expected to be evenly distributed quarter on quarter.

Capital requirements at Macraes for 2022 are principally related to sustaining capital, with growth capital mainly related to the Golden Point Underground (“GPUG”) and expansionary drilling. For the remainder of the year, the operation will source ore from multiple open pits and from Frasers Underground plus GPUG, which will continue to ramp-up over the next two years. GPUG development advance rates are steadily increasing to approximately 600 metres per month by the end of the second quarter, ahead of stoping which is due to commence in the third quarter. A full development advance rate of an estimated 800 metres per month is expected by the end of the year. By the start of 2023, GPUG anticipates producing on average 80,000 tonnes of ore per month and will become the primary source of underground ore at Macraes.

Beyond 2022, production at Macraes is expected to remain steady between 140,000 and 160,000 ounces over 2023 and 2024 while costs and capital requirements are expected to remain flat over the next two years from continued stoping and development of GPUG.

2021 Full Year Results Webcast

The Company will host its 2021 Full Year Results Webcast at 5:30pm on Wednesday February 23, 2022 (Toronto, Eastern Standard Time) / 9:30am on Thursday February 24, 2022 (Melbourne, Eastern Daylight Time)

Authorised for release to market by OceanaGold Corporate Company Secretary, Liang Tang.

About OceanaGold

OceanaGold is a multinational gold producer committed to the highest standards of technical, environmental, and social performance. For 30 years, we have been contributing to excellence in our industry by delivering sustainable environmental and social outcomes for our communities, and strong returns for our shareholders.

Our global exploration, development, and operating experience has created a significant pipeline of organic growth opportunities and a portfolio of established operating assets including Didipio Mine in the Philippines; Macraes and Waihi operations in New Zealand; and Haile Gold Mine in the United States of America.

Competent/Qualified Person’s Statement

The reserves in this release were prepared in accordance with the standards set out in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’ (“JORC Code”) and in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators (“NI 43-101”). The JORC Code is the accepted reporting standard for the Australian Stock Exchange Limited (“ASX”).

Information relating to Haile open pit reserves in this document have been verified by, is based on and fairly represents information compiled by or prepared under the supervision of G. Hollett, a Professional Engineer (P.Eng) registered with Engineers and Geoscientists of British Columbia (EGBC) and an employee of OceanaGold. Mr Hollet has sufficient experience that is relevant to the style of mineralisation and type of deposit under consideration and to the activity being undertaken to qualify as a Competent Person as defined in the JORC Code and is Qualified Persons for the purposes of the NI 43 101. Mr Hollet consents to the inclusion in this public report of the matters based on their information in the form and context in which it appears.

Cautionary Statement for Public Release

Certain information contained in this public release may be deemed “forward-looking” within the meaning of applicable securities laws. Forward-looking statements and information relate to future performance and reflect the Company’s expectations regarding the generation of free cash flow, achievement of guidance, execution of business strategy, future growth, future production, estimated costs, results of operations, business prospects and opportunities of OceanaGold Corporation and its related subsidiaries. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects” or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “estimates” or “intends”, or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved) are not statements of historical fact and may be forward-looking statements. Forward-looking statements are subject to a variety of risks and uncertainties which could cause actual events or results to differ materially from those expressed in the forward-looking statements and information. They include, among others, the outbreak of an infectious disease, the accuracy of mineral reserve and resource estimates and related assumptions, inherent operating risks and those risk factors identified in the Company’s most recent Annual Information Form prepared and filed with securities regulators which is available on SEDAR at www.sedar.com under the Company’s name. There are no assurances the Company can fulfil forward-looking statements and information. Such forward-looking statements and information are only predictions based on current information available to management as of the date that such predictions are made; actual events or results may differ materially as a result of risks facing the Company, some of which are beyond the Company’s control. Although the Company believes that any forward-looking statements and information contained in this press release is based on reasonable assumptions, readers cannot be assured that actual outcomes or results will be consistent with such statements. Accordingly, readers should not place undue reliance on forward-looking statements and information. The Company expressly disclaims any intention or obligation to update or revise any forward-looking statements and information, whether as a result of new information, events or otherwise, except as required by applicable securities laws. The information contained in this release is not investment or financial product advice.

www.oceanagold.com | Twitter: @OceanaGold

Source: Junior Mining Network