OceanaGold: After A 50% Drop, There Could Be Value In This Mid-Tier Gold Producer

Summary

- OceanaGold continues to suffer after having to close its Didipio gold-copper mine in the Philippines last year.

- Despite the loss of Didipio, Oceana is still a 400,000-ounce-a-year gold producer with a market cap of only $950 million.

- The company’s remaining core assets are in New Zealand and the US, top-tier jurisdictions.

- Costs are higher than ever across Oceana’s operations, but still provide a healthy profit margin at current gold prices.

- New growth opportunities at Waihi and Haile show long-term upside.

OceanaGold is a diversified, mid-tier gold producer with operations in New Zealand, the US and the Philippines. The company has been a massive underperformer during a gold bull market due to a dispute at its Didipio mine in the Philippines. This has cut overall gold production by 25% and sent the stock crashing.

We review OceanaGold solely on its remaining operations, ignoring Didipio, to see if there’s potential value at these levels.

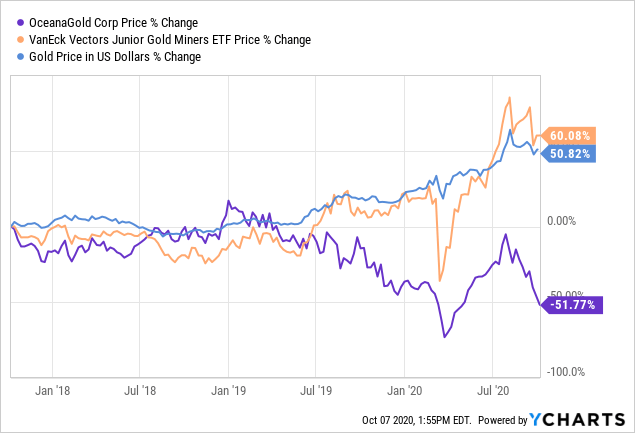

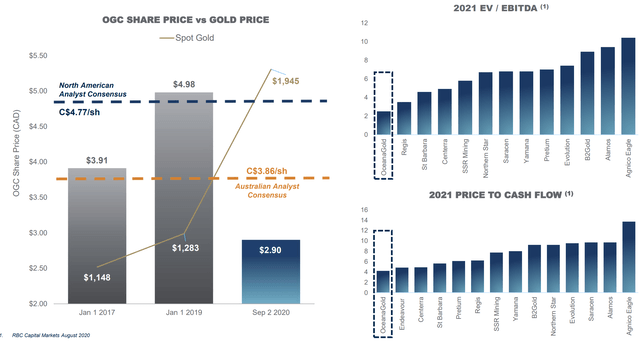

Looking at the share price performance over the past three years, it’s clear to see the company has underperformed its peer group and the price of gold since the problems at Didipio began last July. OceanaGold has failed to take advantage of a strong move in gold that led to the yellow metal hitting record-high levels in August.

Three-year share price performance

(Source: YCharts)

Didipio: A High-Quality Mine That Doesn’t Seem to be Coming Back Anytime Soon

A key reason for the massive underperformance of Oceana has been a government and social dispute in the Philippines over the company’s Didipio gold-copper mine, which has been on care and maintenance since July 2019.

Didipio was one of the company’s better assets before the shutdown, churning out 130,000 ounces of gold and 15,000 tonnes of copper annually at $650/oz all-in sustaining costs (AISC), by far the lowest among the group’s four operations. It was previously an open-pit mine that has transitioned to underground mining, with a total resource of 1.7 million ounces gold and 200,000 tonnes of copper. The low costs at Didipio helped keep the group’s aggregate AISC below $900/oz, while some of its higher-cost mines struggled to be profitable. Without Didipio, the company’s AISC is now averaging $1,000-1,100/oz, which is one of the higher-cost profiles in the sector.

2019 production and cost guidance

(Source: Company news release)

In June of last year, OceanaGold started reporting on issues with its renewal process of the Financial or Technical Assistance Agreement (FTAA) required to operate the Didipio mine. The company had initially submitted a renewal application in 2018, and at first reassured shareholders that there would be no impact on Didipio. Later, in July, the provincial government moved to block access to the site alongside local anti-mining protesters, and the company ultimately suspended operations.

Environmental and social disputes like these could drag on forever, and Oceana’s claims that the governor of the Nueva Vizcaya province has no jurisdiction over the mining operation hasn’t stopped the local government from continuing to block the mine. As a next step, the company needs ratification of the FTAA renewal at the national level, which may be difficult given President Duterte’s long-standing opposition to mining, which has hampered other projects in the country, including a country-wide ban on open-pit mining. Even if the company is able to get its permit renewed by the President, local protesters and the provincial government may continue to oppose and blockade the mine.

If OceanaGold can find a way to resolve the dispute, investors could look forward to a material rerating opportunity. The company may also look to sell the asset, but would not be getting fair value for the operation unless there was some indication that new ownership could resolve the dispute. A Chinese gold producer may be the right type of acquirer, otherwise we see it unlikely that any other buyers would contemplate taking on Didipio’s ongoing problems. A sale would leave Oceana a smaller company, but one with a much more appealing jurisdictional focus for Western investors.

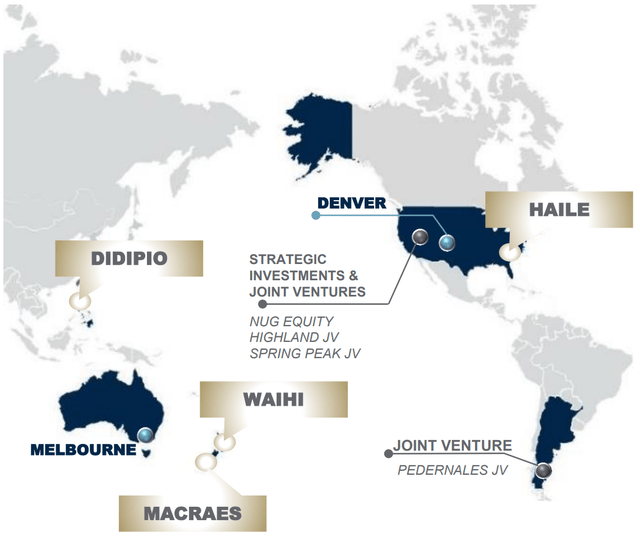

Portfolio overview

(Source: Company presentation)

The Rest of the Portfolio: Solid Operations in Top-Tier Jurisdictions

Ignoring Didipio and looking at the company’s other core projects, its future looks much brighter. The rest of Oceana’s portfolio is located in tier-one jurisdictions, including the Macraes and Waihi operations in New Zealand and the Haile mine in South Carolina. Altogether, these operations are expected to produce 400,000 ounces per year, and the company has expansion opportunities at each mine that will underpin future production and margins.

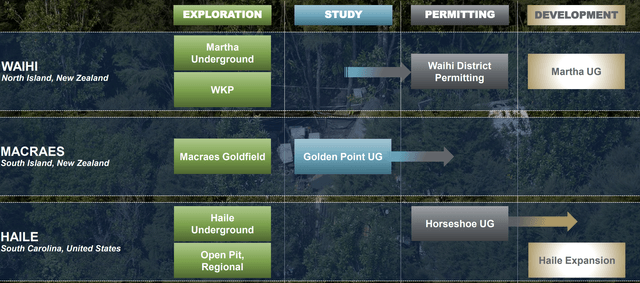

Organic growth pipeline

(Source: Company presentation)

In July, the company released a Preliminary Economic Assessment on the Waihi district, outlining the potential of several projects, including the Martha underground expansion, WKP underground, Gladstone open pit and a cutback of the existing Martha open pit.

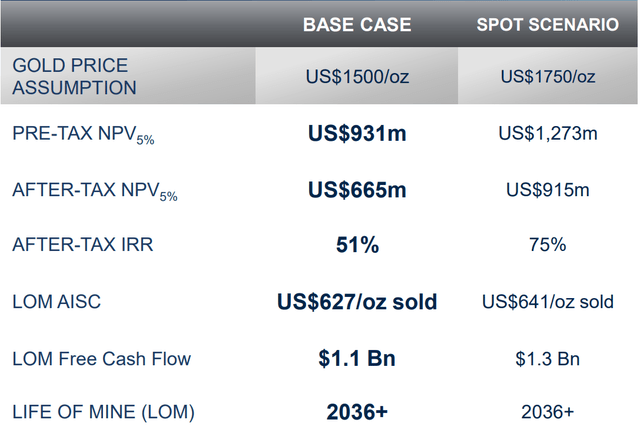

The study showed very positive economics at conservative metal prices of $1,500/oz, compared to today’s levels around $1,900/oz. The combined operation was estimated to have an NPV of $665 million and an IRR of 51% based on capital costs of $447 million spread out over eight years. With average annual production around 150,000 ounces from all deposits over 15 years at low AISC of $627/oz, this project alone could underpin a large portion of the company’s current valuation, but as we’ll see later, the market is heavily discounting the net asset value of Oceana’s portfolio.

Waihi district PEA highlights

(Source: Company presentation)

The Martha underground expansion is in progress and remains on schedule, with management projecting first production in the second quarter of next year. The company also received mining permits for WKP in August, a small but high-grade underground gold project with indicated resources of 421,000 ounces at 13.4 g/t and inferred resources of 717,000 ounces at 12.0 g/t.

Aside from the shock of losing Didipio, another reason for the recent drag on the share price has been higher operating costs at Haile and Macraes. The company reported a lacklustre $1,061/oz AISC in 2019 and is guiding for $1,050-1,100/oz this year (although this is partly due to the effects of COVID-19 on their operations). Hopefully, new management can bring the company’s AISC down to below $1,000/oz.

While Macraes is an older mine closer to the end of its life, Haile’s recent underperformance has been more frustrating given the initial projections for this new operation, with very high AISC around $1,250/oz. While a savvy acquisition by management near the bottom of the market in 2015, the mine has so far failed to live up to expectations since going into production in 2017, suffering higher stripping costs and lower grades. One commonly cited issue is the heavy rainfall that the area experiences, but as the operation matures, we believe management will be able to turn the mine around.

If management can return Haile to the cost profile seen in 2018 of $900/oz, and with 4.4 million ounces of gold and a 13-year mine life, Haile should boost Oceana’s value for years to come. An updated mine plan released last month showed an NPV of $892 million at a $1,500/oz gold price assuming $800/oz AISC over the mine life, with production reaching 250,000 ounces per year from 2023 to 2027. If management can execute this plan at Haile, it will be a significant boost to Oceana’s value.

Underperformance Has Led to a Depressed Valuation Compared to Peers

espite issues in the Philippines and a higher cost profile, a market capitalization of only $950 million for a 400,000 ounce per year multi-asset producer appears to be a bargain in a strong gold market like this.

While initially participating in the precious metals rally and reaching a recent high of C$4/share on July 27, the share price has since dropped 50%. Compared to a peer group of mid-tier gold producers, the company is now trading at a significant discount on 2021 estimates. Oceana could be due for a rerating even without a resolution at Didipio, especially if the company can bring its costs down in the coming quarters and successfully bring the Martha underground project on-line.

Combining the recent after-tax NPV estimates for Haile ($892 million), Waihi ($665 million) and Macraes ($325 million) at $1,500/oz gold prices, the company’s portfolio value is $1.9 billion, without factoring in a potential restart at Didipio. This works out to a price-to-net asset value ratio of around 0.5 times, while most of its mid-tier peers are trading between 0.9 and 1.4 times, implying clear upside for OceanaGold if it can get back on track.

Valuation disconnect

(Source: Company presentation)

On September 29th, the company announced a C$150 million bought deal at C$2.06 per share, a 9% discount from its trading level that day. The stock promptly dropped 9% the next day and has been trading around those levels since.

Before the financing, Oceana’s balance sheet was relatively healthy with $181 million cash and $317 million in debt, for a total net debt of $136 million. With the financing expected to close in the next few weeks, the company will be close to zero net debt.

Concluding Thoughts

OceanaGold continues to suffer from the overhang of a dispute in the Philippines that has led to the company’s lowest cost mine being put on the shelf for over a year. Didipio continues to be on care & maintenance, and at this time, we assign no value to the operation. The permit renewal is currently in the hands of the government, however, there is no timeline on a decision.

The rest of its mines are reporting higher costs in recent quarters, but we believe these costs will come down, and at current gold prices, the company’s margin is still good.

Despite the negative developments over the past year, Oceana is still a 400,000-ounce-a-year gold producer with a market cap of only $950 million and a healthy balance sheet. A management turnaround and new growth initiatives at its operations in tier-one countries could lead to a rerating for this undervalued mid-tier producer.

Source: Seeking Alpha