Amur Minerals And Garibaldi Resources: 2 Mining Juniors To Benefit From A Nickel Boom As LME Inventories Fall Sharply

By Matt Bohlsen

LME inventory levels fell last week, the most in 40 years. Nickel price forecasts all see higher nickel prices in the next decade.

Two nickel juniors that can do very well if nickel prices spike higher.

Risk and reward are both higher when investing in junior miners.

I do much more than just articles at Trend Investing: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

This article first appeared on Trend Investing on October 10, 2019; therefore all data is as of this date.

Two recent events have caused nickel prices to rise as inventories fall:

- The Indonesian nickel ore export ban set to begin January 2020.

- Nickel mining indefinitely suspended in southern Philippines. 27% of overall Philippine nickel ore exports are from this area.

Given that Indonesia supplies 28% and Philippines 17% of global nickel supply, these supply cuts are causing nickel prices to surge (up 50% in the past 3-4 months). Assuming nickel demand can hold strong, 2020 should see nickel in further structural deficit and inventory levels wind down even further. That should mean higher nickel prices ahead.

LME inventory levels fell last week, the most in 40 years

This past week, nickel inventories at the London Metals exchange have dropped dramatically as shown in the graph below. The drop was caused by some large purchases by China’s Tsingshan Holding Group Co.

A Mining.com article states:

The move last week was surprisingly sharp – the nearly 25,000 tons that left the warehouses was the biggest decline in the four-decade history of the nickel contract… While the LME’s warehouse network is designed as a last-resort source for exactly this type of supply crisis, the scale of buying could raise concerns about a potential shortfall if the drawdowns continue.

The LME’s record of orders show that another 75,000 tons of metal are scheduled to be delivered out. People familiar with Tsingshan’s deals declined to specify how much more metal the company may be seeking to withdraw.

Reading the above quote suggests we may be about to face a nickel supply crisis. If this were to be the case, nickel prices would spike further and move above US$10/lb. Promising nickel juniors could benefit the most as they become more economic with higher nickel prices.

In my September 5, 2019, article: “Nickel Is Hot Right Now – The Nickel Boom May Have Just Begun”, I quoted:

Today LME nickel inventory is at 153,000 tonnes and has been falling steadily for some time now. The Indonesia export ban could easily send nickel inventories back below 50,000 tonnes in 2020 and cause another huge nickel price spike.

“Demand for nickel in the EV space is expected to total 36,000 tonnes in 2018…..That figure is expected to surge to 350,000-500,000 tonnes by 2025.” That’s more than a tenfold increase, in just 7 years. Wow! The best source of nickel sulphate will come from the nickel sulphide miners.

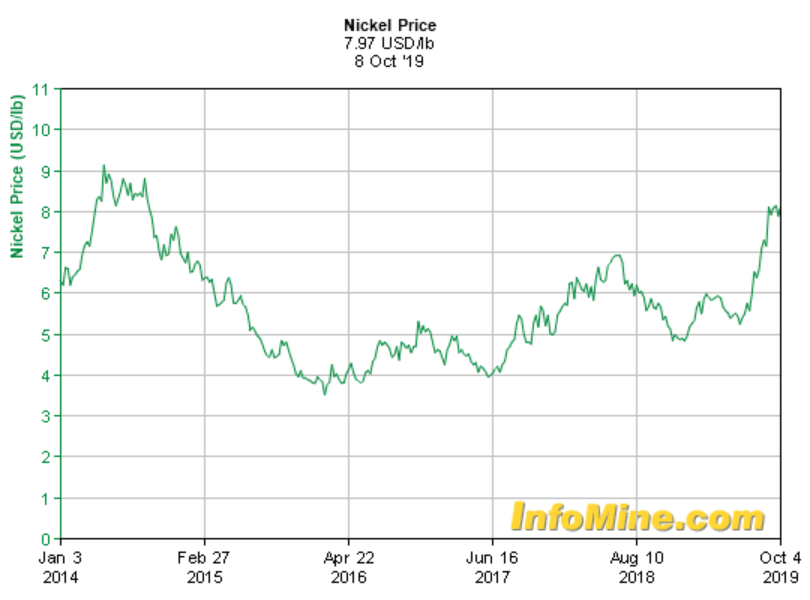

Nickel 5-year price chart

Source: InfoMine

Nickel price forecasts all see higher nickel prices in the next decade

Source

Two nickel juniors that can do very well if nickel prices spike higher

The two juniors below were chosen as they have large upside potential should nickel prices spike higher and if they advance to production quickly. Both are nickel sulphide ore, so CapEx to reach production should be lower than laterite ore projects. Also, costs of production to produce class 1 nickel sulphate should end up reasonable (helped by sulphide ore), depending on grades and by-product credits.

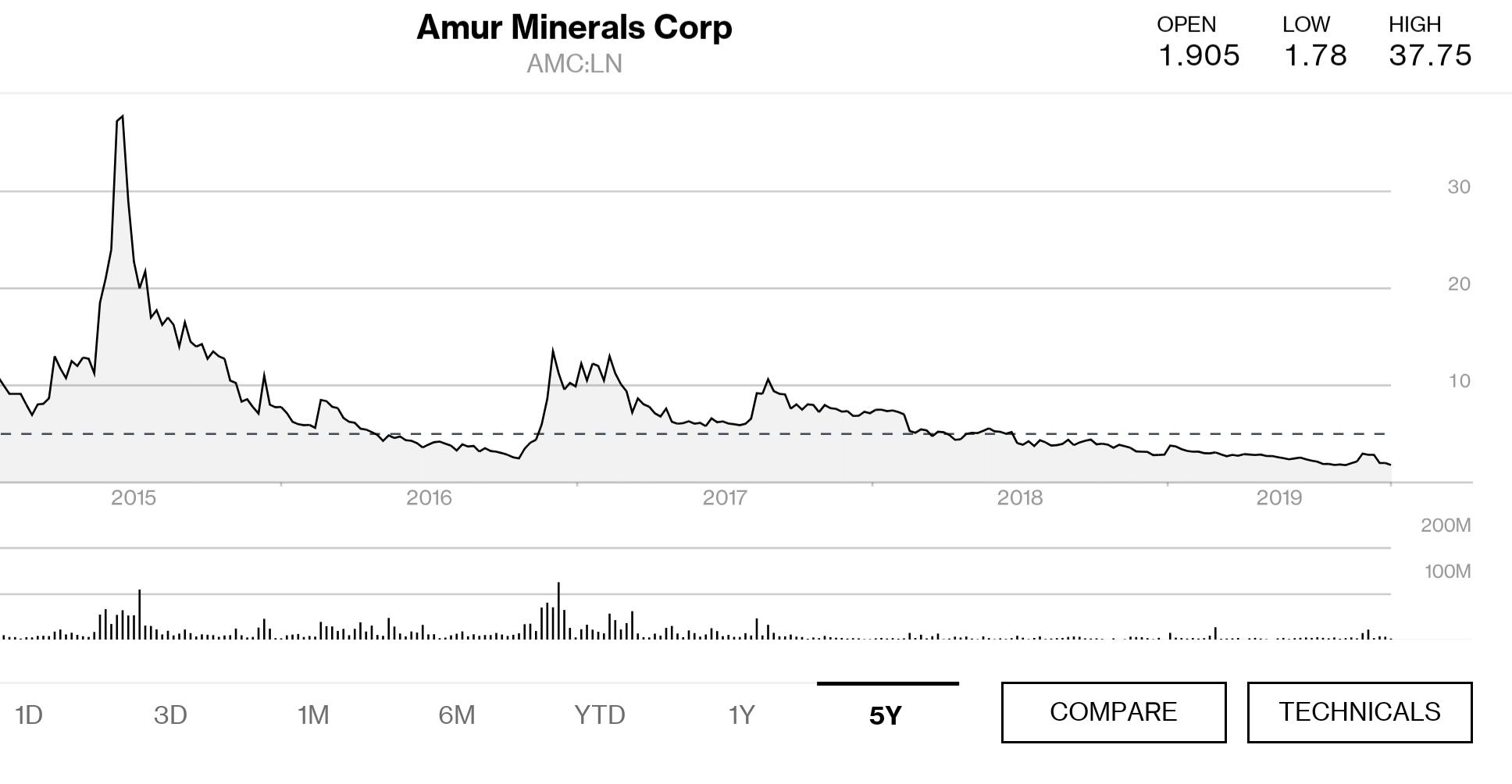

1) Amur Minerals Corp. [LSE:AMC] [GR:A7L] (OTCPK:AMMCF) – Price = 1.90 GBP

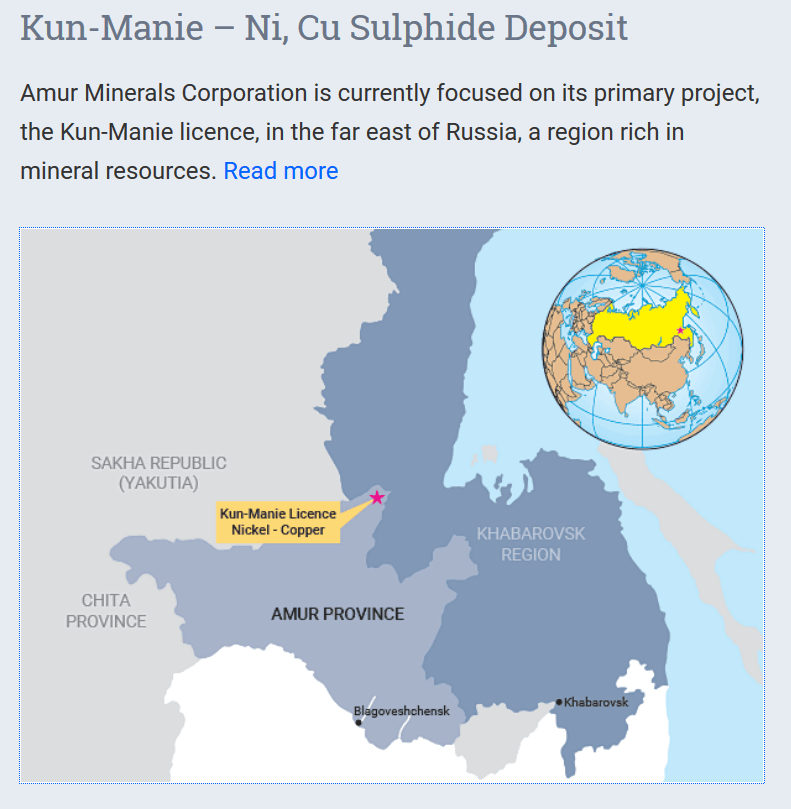

Amur Minerals Corp. [“AMC”] is an English company with large sized nickel-copper sulphide projects in Russia. Their flagship is the massive low grade (sulphide ore) Kun-Manie Nickel-Copper Project in the Amur Oblast region of Russia.

Amur Minerals massive Kun-Marie Nickel-Copper Sulphide deposit

Source

The Project contains economic amounts of nickel, copper, cobalt, platinum, and palladium. The Company states:

- Average of 1.02% nickel equivalent grade (Ni, Cu, Co, Pl +Pd) based on 9 March 2018 metal pricing.

- The average nickel grade is 0.75%, copper is 0.21%, cobalt is 0.015%, platinum is 0.16 g/t and palladium is 0.17 g/t. Additional minor amounts of gold and silver will also be recovered but have not been estimated.

- 1,581,000 nickel equivalent tonnes.

- More than 76% of the resource is identified as Measured and Indicated.

- By sulphide nickel equivalent tonnage, the present MRE [Measured Resource estimate] places Amur within the 3 largest publically listed greenfield nickel sulphide resource companies in the world and the largest undeveloped nickel sulphide deposit immediately adjacent China, Korea and Japan.”

The project is in the development stage and has a mining license to 2035 which can be extended.

Amur states:

The resource ranks AMC among the largest undeveloped nickel sulphide companies in the world having 155.1 million ore tonne resource contained within four deposits. Containing recoverable nickel, copper, cobalt, platinum and palladium, the average nickel equivalent grade is 1.02%. The total nickel equivalent tonnage is 1.58 million tonnes.

February 2019 Preliminary Feasibility Study [PFS] results

The February 2019 PFS presented two options:

- Toll Smelt [TS] Option – Post tax NPV (10%) $614.5 million, post tax IRR 29.3%. C1 cash cost US$3.87/lb. Initial CapEx US$570m. LOM 15 years.

- Furnace Flash Smelter [FFS] Option – Post tax NPV (10%) $987.4 million, post tax IRR 34.7%. C1 cash cost US$2.45/lb. Initial CapEx US$695m. LOM 15 years.

PFS Summary

Market cap is GBP 14m. 4-Traders shows an estimated 2019 debt of $12.1m. I was unable to find an analyst price target. Due to their location and somewhat lower grade, the market cap is very low. However, as nickel prices rise, the project’s viability grows rapidly giving excellent nickel price optionality. Also, the by-products give a reasonably low cost of production. CapEx is reasonable especially given that the possibility of mine life can be extended. Production start up is aimed for 2023, so some patience required.

Recent significant insider buying by Non-Executive Director Tom Bowens of 7,527,604 new ordinary shares for GBP 162,972 (at GBP 2.165) is also very encouraging.

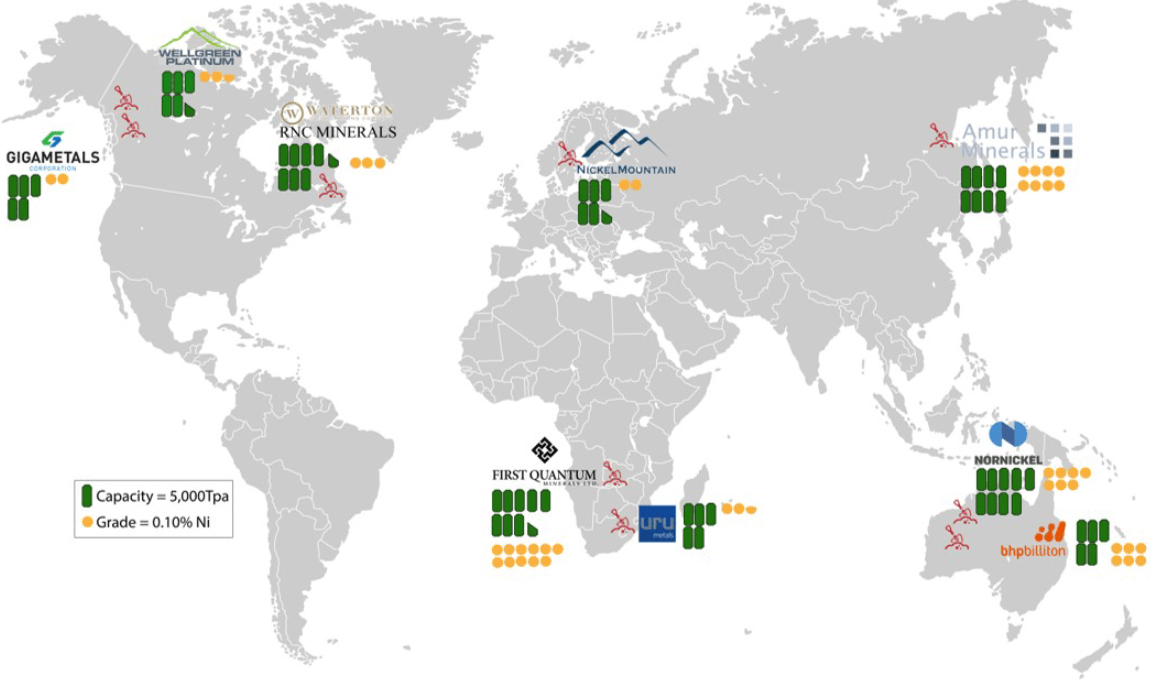

Nickel sulphide projects with >20,000t p.a. likely to come into production over the next 5 years

Source: Amur Minerals Corp. company presentation

You can view the latest company presentation here.

I like Amur Minerals due to their very low market cap and optionality to a higher nickel price. Also that they have an advanced project which is ‘among the largest undeveloped nickel sulphide’ resources globally, located close to Asia. Risk is high due to the somewhat earlier stage (post-PFS) and Russian location. I rate Amur Minerals as a strong speculative buy.

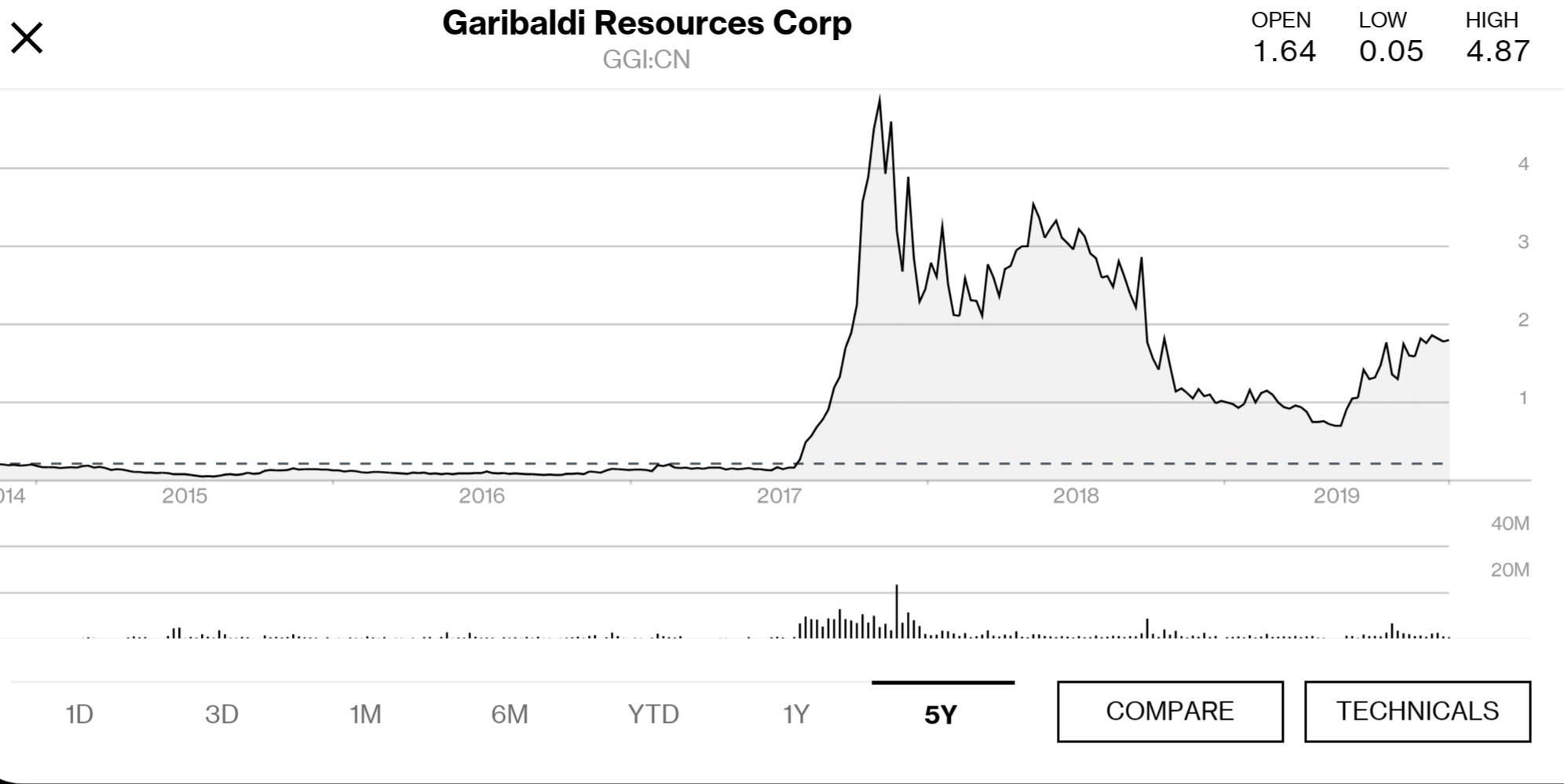

2) Garibaldi Resources Inc. [TSXV:GG] (OTC:GGIFF) – Price = CAD 1.61

Garibaldi Resources made British Columbia’s [BC] exploration history in 2017 with the discovery of NW British Columbia’s first magmatic nickel massive sulphide featuring 7 metals – nickel, copper, cobalt, platinum, palladium, gold, and silver. Garibaldi owns 200 sq km in the Eskay Camp region known for large gold discoveries. Their flagship project is the Nickel Mountain Project. Garibaldi also has several other projects (Canada – King, Palm Springs Property, Red Lion, Grizzly; Mexico – La Patilla, Rodadero, Tonichi, Iris) as you can read here.

Source: Seeking Alpha