Pressure builds on China’s raw materials supply chains

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

Worker in machinery factory, China. Stock image

China is ready to move on from the coronavirus and get back to business as usual.

“With the spread of covid-19 under control, we should actively carry out the resumption of work and production,” President Xi Jinping said this week.

Xi’s comments, reported by state media under the headline “Chinese president unpauses China’s economy”, were made during a tour of Zhejiang province. (CGTN, part of China Media Group, April 2, 2020)

As ever, Xi’s whistle-stop tour was an exercise in subliminal messaging. Those comments were made during a visit to an auto parts supplier in the Daqi industrial park in the city of Ningbo.

He also dropped in on Ningbo Zhoushan port, one of the world’s busiest, and praised it for getting throughput back to pre-coronavirus levels.

“AS THE CORONAVIRUS SPREADS, SO TOO DO THE LOCKDOWNS ON ACTIVITY IN KEY SUPPLIER COUNTRIES SUCH AS CHILE, PERU, SOUTH AFRICA AND INDONESIA”

The political messaging, however, masks the fragility of China’s metals raw material supply chains.

As the coronavirus spreads, so too do the lockdowns on activity in key supplier countries such as Chile, Peru, South Africa and Indonesia.

China has rapidly built out its metals refining capacity over the last decade but at the cost of needing ever more imported raw materials to feed its smelters.

Some of those supply chains are now starting to creak.

Lockdown lottery

The metallic spectrum of China’s raw materials imports is highly differentiated, depending on the origin and number of supplier countries.

Ongoing emergency lockdowns in Chile and Peru, for example, place at risk flows of copper, zinc and lead concentrates.

Chile and Peru accounted for 55% of China’s inbound cargoes of copper concentrate in 2017, the last year China’s customs department published a full breakdown of metal imports.

“CHILE AND PERU ACCOUNTED FOR 55% OF CHINA’S INBOUND CARGOES OF COPPER CONCENTRATE IN 2017”

The two countries are also major suppliers of zinc concentrate, but so too is Australia, where mining operations have so far been less affected.

The pressure on supply chains is accentuated in metals such as chrome, where production is concentrated in one particular country.

South Africa last year accounted for 83% of China’s imports of chrome ore, a core input for stainless steel producers.

The country has ordered all mines and furnaces closed from March 26 with the result that local producers Samancor, Tharisa and Glencore-Merafe Chrome have declared force majeure on deliveries.

Cobalt supply is dominated by the Democratic Republic of Congo, where producers are proactively reducing output and shipping routes via South Africa risk being disrupted by port closures.

Stressed supply chains

The effects of such country-by-country lockdowns are most acute on those raw material supply chains that were already under pressure, such as nickel.

Indonesia, which has historically been a key supplier of nickel ore to China’s nickel pig iron (NPI) producers, has this year banned all unprocessed ore exports.

The market was looking to the Philippines to pick up some of the slack but that country has just suspended mining operations in the southern province of Surigao del Norte, home to most of the country’s nickel mines.

It has also stopped the entry of foreign vessels to the province, risking a full cut-off of shipments.

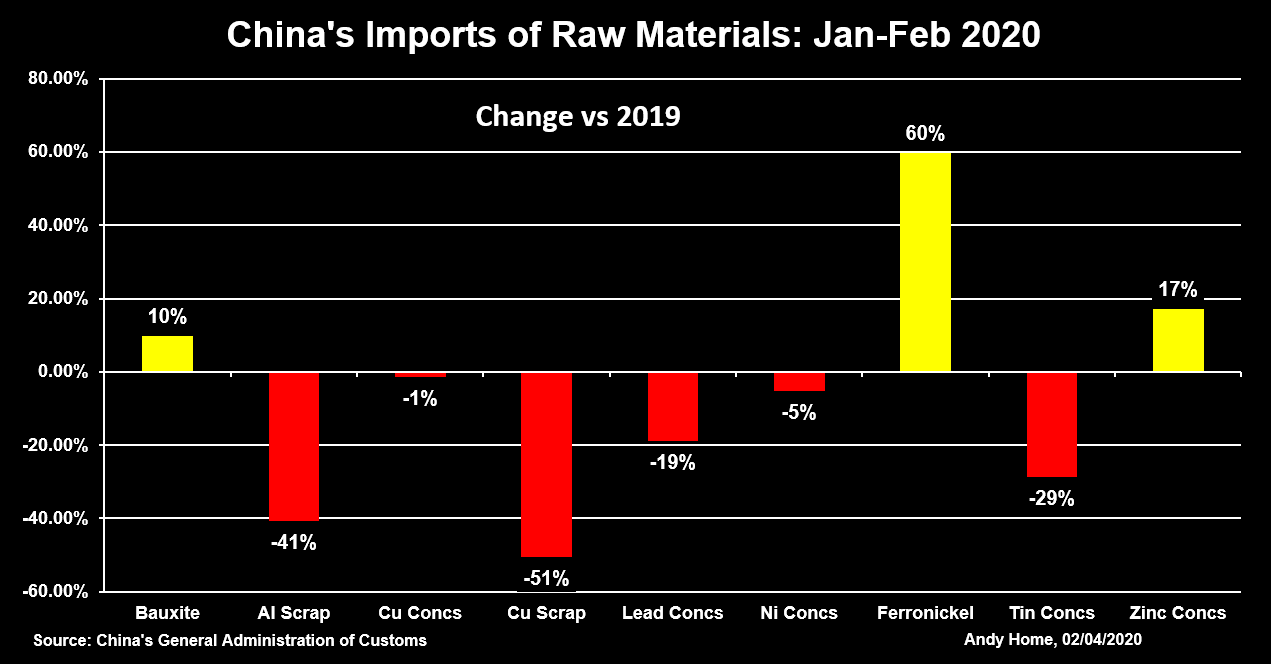

China’s nickel ore imports were already down by 5% in the first two months of this year due to the combination of the Indonesian ban and the seasonal drop in Filipino production over the rainy season.

Unless either country reverses its policy decisions, imports of ore are going to fall much harder.

Some compensation may come from accelerated flows of Indonesian NPI direct to China’s stainless steel producers. China’s ferronickel imports, a customs code that includes NPI, jumped by 60% year-on-year in January-February.

But the market was already sceptical that Indonesian NPI could fill the ore gap and continued exports are dependent on whether Indonesia can maintain mining operations as it rolls out increasingly draconian anti-virus restrictions on movement.

Higher metal imports

Tin is another metal with a stressed Chinese supply chain.

The country’s smelters rely on imports of tin concentrates from Myanmar, where production has been steadily declining over recent years as tin miners exhaust easily-exploited resources.

China’s imports of tin concentrates fell by 20% last year and were down another 29% in January-February as border controls and restrictions on movement squeezed flows of raw material.

With several Chinese smelters also locked down over the peak of the coronavirus outbreak in China, the country’s shortfall has translated into accelerated imports of refined tin metal.

China imported 1,660 tonnes of tin in January-February, compared with 3,000 tonnes and 2,500 tonnes for the whole of 2019 and 2018 respectively.

It flipped to being a net refined tin importer for the first time since 2017.

It may be a template for how raw materials’ disruption translates into higher imports of refined metal, upending a long-running trend of increased Chinese self-sufficiency at the metal stage of the production value chain.

However, that assumes that flows of refined metal aren’t subject to the same levels of lockdown and shipping problems that are already stressing raw materials chains.

Demand fears still dominate

China’s increased draw on refined tin from the international market hasn’t done anything to help tin prices.

London Metal Exchange tin sank to a decade-low of $12,700 last month and is currently trading at $14,550, still the lowest price level since the base metals cyclical trough on 2016.

That’s because all the base metals markets are more focused right now on the collapse in global demand, both at the first-use fabricator and the end-use consumer stage.

Supply disruptions due to mining lockdowns and logistics bottlenecks are still playing catch-up with the demand shock rippling around the world.

Moreover, Chinese importers are probably carrying sufficient supplies of raw materials to ensure production over the short term.

But the longer lockdowns go on, and there are plenty of indications that they will be extended for as long as it takes to control the spread of the virus, the greater the potential for supply chain disruption.

As the biggest buyer of metallic raw materials, this is a ticking time-bomb for China’s metals producers.

President Xi may be keen to stress that China is open for business as usual, but it’s far from being business as usual for miners around the world.

The pressure on the country’s raw materials supply chains is only going to get worse.

(Editing by Susan Fenton)

Source: Mining dot Com